Good Outcomes and Good Decisions Are Not the Same Thing

Picture two traders at the end of the same month. Trader A finishes up 3%. On paper, it looks like a success...right? Beneath the number, they sized up after a winning streak, moved a stop because the trade was "almost there," and caught a lucky runner on a setup they had never backtested. Meanwhile, Trader B finishes up 4%. Every trade followed the plan. Losses were cut at -1R. Winners reached +2R. Position sizing stayed consistent regardless of what happened the trade before. Most traders would prefer to have Trader A's result. Experienced traders would rather have Trader B's process.

The problem with looking only at P&L is that it shows the outcome, not the decisions behind it. It does not reveal whether profits came from skill or luck or whether losses came from poor execution or a strategy playing out exactly as expected. Focus solely on results and you reinforce bad habits while overlooking good ones.

Three traps almost every trader falls into at review time:

– Green week = good trading. Seven profitable days can hide negative expectancy or one outlier masking a weak system.

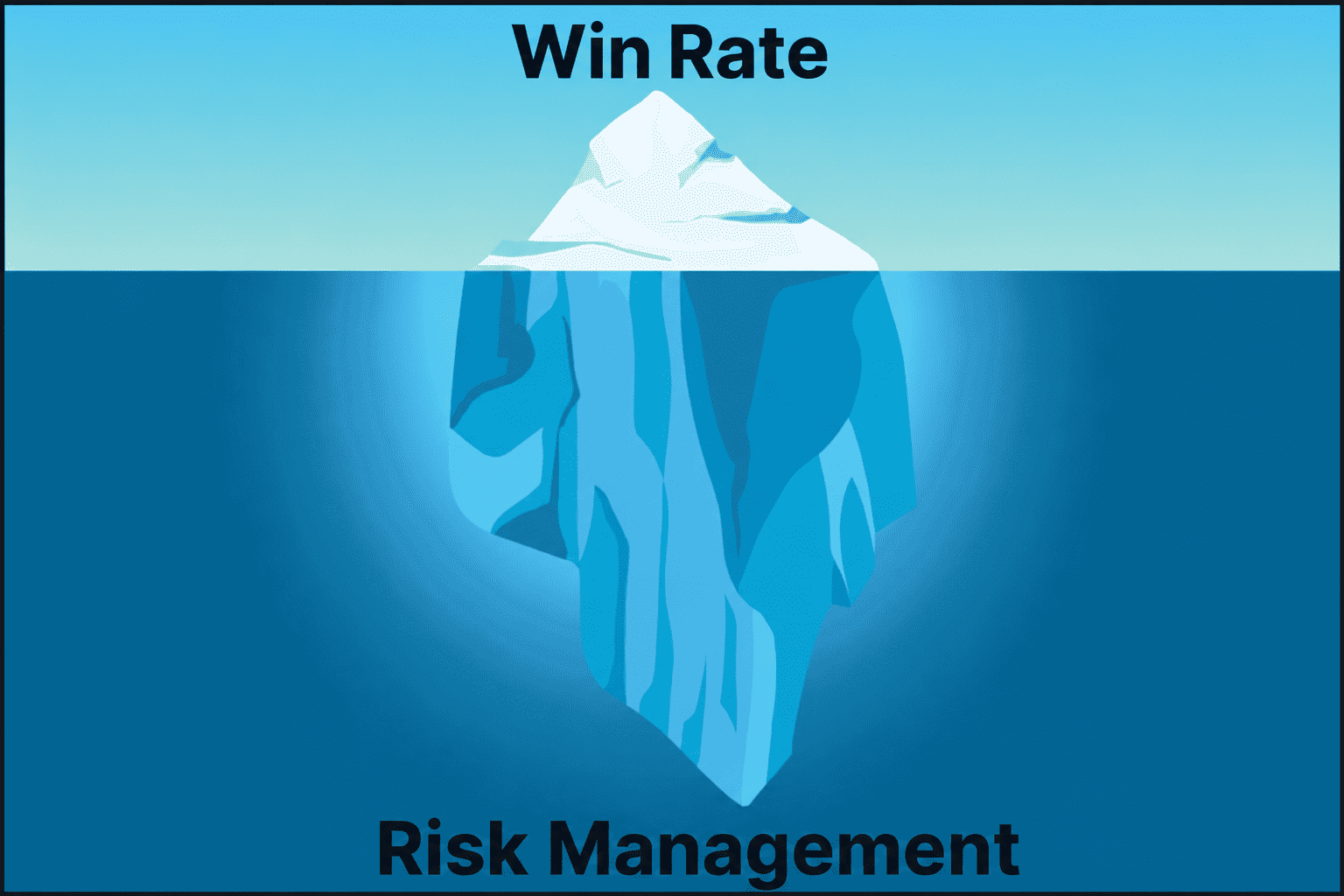

– High win rate = edge. An 82% win rate loses money when average losses are five times average wins. Arithmetic, not psychology.

– Best trade = proof of strategy. One +8R spike on a +0.1R system does not validate the setup. It validates overconfidence — often with larger size on the next entry.

The dangerous trade is not always your biggest loss. Sometimes it is the win that teaches you the wrong lesson.

Separate what happened from what you did. Did size match the rule? Did you exit on plan — or because the candle made you nervous? Those answers do not live in win rate or monthly P&L. They live in your trade journal — when you track mistakes and decision quality alongside the result.

Key takeaway: Review your performance through multiple trade metrics, for a well rounded view. The goal is not simply to know whether you made money. It is to understand whether you traded well.